As the banking industry continues to face a crisis due to the collapse of Silicon Valley Bank, investors are seeking more stable and liquid investment options. One such option is money market funds, which invest in short-term securities like government bonds, certificates of deposit, and commercial debt. However, these funds are not without risks, especially when experiencing a large wave of investors all at once.

Record Inflows into Money Market Funds

Since the Federal Reserve began raising interest rates in 2015, the amount of money invested in money market funds has increased by $400 billion. Currently, a record $5 trillion is invested in these funds with retail money market fund assets reaching $1.86 trillion as of March 22. Investors have been piling into government money market funds, particularly those that hold U.S. Treasuries. Such inflows indicate a continuation of flight to quality by institutions and retail investors following the Silicon Valley Bank banking crisis.

Yields Increase Due to Fed’s Rate Hikes

Money market funds have seen yields increase due to the Fed’s rate hikes that affected SVB’s loan portfolio and caused people to leave less established banks. Crane 100 Money Fund Index is posting an annualized seven-day current yield of 4.54% as of March 27.

JPMorgan strategists note that Government Money Market Funds have a yield advantage due to their investments in Fed’s reverse repos and Tbills. Tax-exempt money market funds hold municipal market securities and provide income exempt from federal income taxes. Some state-specific money market funds make sense for residents in high-tax jurisdictions.

Risks Associated with Money Market Funds

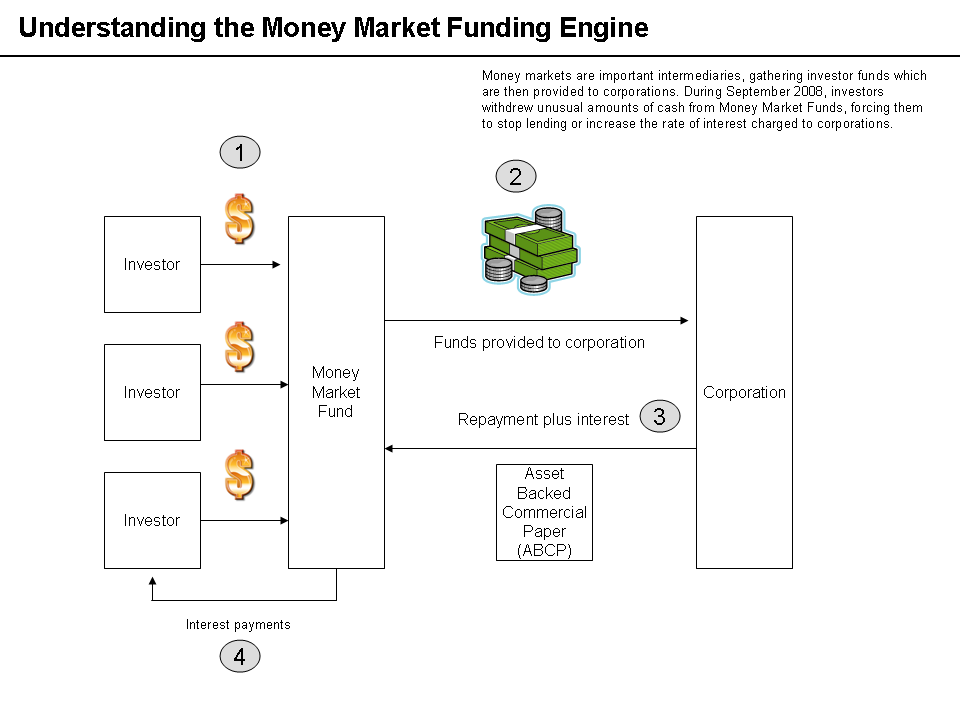

Money market funds are deeply interconnected with the wider financial system and can amplify existing stress in the system. The more money there is invested in these funds, the greater the risk of creating a money-market liquidity crisis, where funds may not have enough cash on hand to meet redemptions.

While money market funds offer relative safety, they do have some risks and are not federally insured. They can be a good place for short-term savings or assets that need to be used in about a year, but are not necessarily a great place for building long-term wealth.

Investors Shift from Smaller Banks to Money Market Funds

Investors are shifting money from smaller banks to money-market funds due to fears about bank safety and higher yields. Since the start of March, $286 billion has flowed into money-market funds, on pace for the biggest month since the depths of COVID-19. Depositors remain nervous and continue to pull deposits from banks, moving cash to money-market funds. Bankrate data shows the top-yielding money-market funds as of Friday, March 24.

It is worth noting that the Federal Deposit Insurance Corporation does not insure cash invested in money market funds, and those funds are also not guaranteed by the US government.

SEC Proposals for Increasing Investor Safety

New proposals for increasing investor safety in money market funds are expected to be unveiled by the Securities and Exchange Commission next month. In light of the risks associated with these funds during a banking meltdown, such proposals would likely focus on mitigating risks associated with a sudden influx of investors that could lead to a liquidity crisis.

In conclusion, while money market funds offer attractive yields and relative safety in these tumultuous times of banking crises, investors need to be aware of their inherent risks. It is essential that potential investors weigh these risks against the potential yields before making any investment decisions. Additionally, regulatory reforms designed to reduce these risks would also benefit investors who regard such investments as relatively safe havens.

Image Source: Wikimedia Commons

{kind=link}